Home Mortgage Tips That Can Make Your Life Easier

Content written by-Burnham EbsenEvery American dreams to own the perfect home of his or her own. If you are searching for your first home but are unsure of the mortgage financing process, this is the perfect article for you. Use the information in the following paragraphs to learn the key tips you need to understand to help you get a great deal on your mortgage financing.

If https://www.wbrc.com/2021/06/25/bunny-stokes-jr-well-known-birmingham-banking-executive-who-paved-way-black-bankers-dies-77/ are considering quitting your job or accepting employment with a different company, delay the change until after the mortgage process has closed. Your mortgage loan has been approved based on the information originally submitted in your application. Any alteration can force a delay in closing or may even force your lender to overturn the decision to approve your loan.

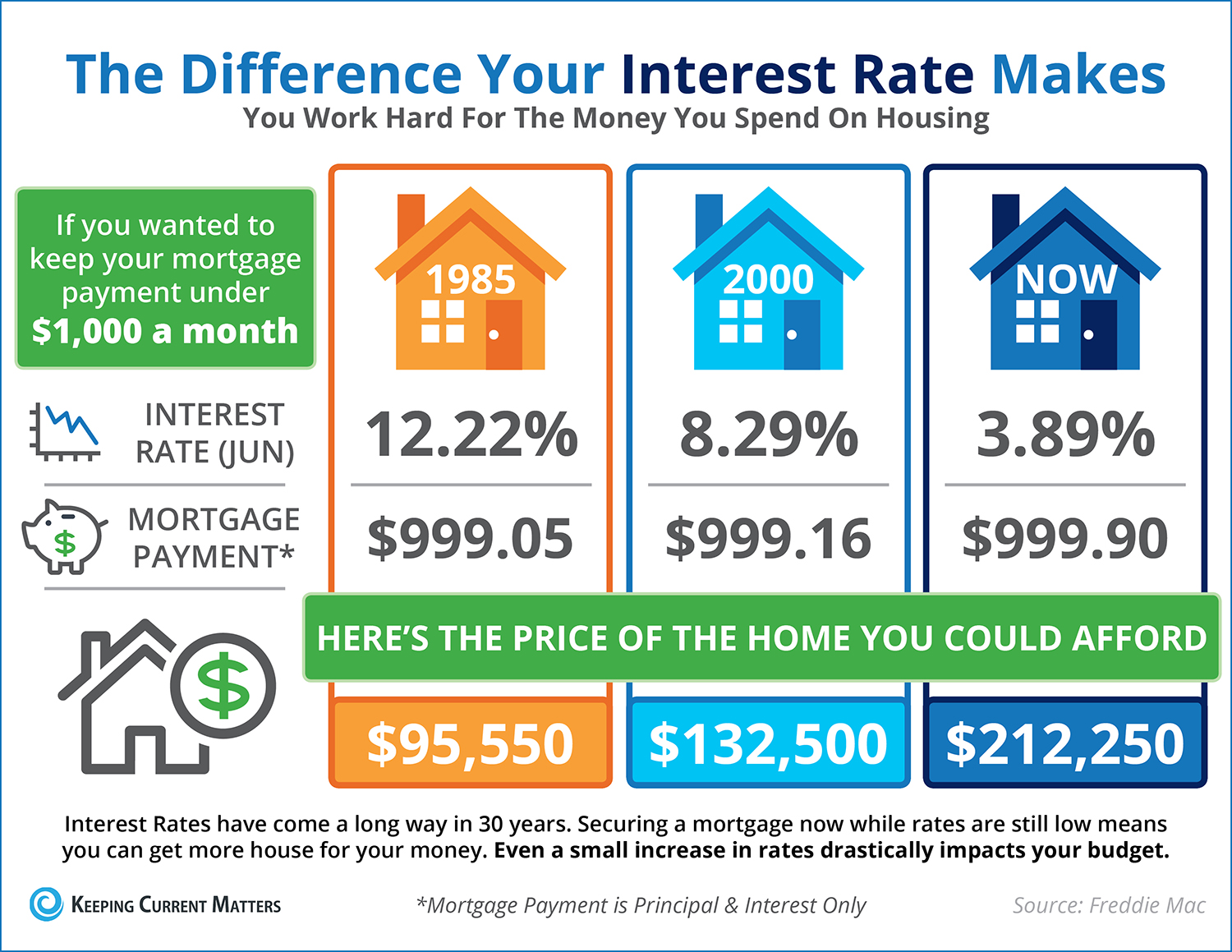

Remember that the interest rate isn't the most important part of a mortgage. You also have to think about closing costs, points and other incidentals. There are different kinds of loan as well. That is why you have to find out as much as you can about what you're eligible for.

Consider hiring a professional to assist you in the process of procuring a new home loan. There is a lot to know about getting a home mortgage and a consultant can help to ensure that you get the best deal possible. They will also make sure that all of the terms of your loan are fair.

Remember that the interest rate isn't the most important part of a mortgage. You also have to think about closing costs, points and other incidentals. There are different kinds of loan as well. That is why you have to find out as much as you can about what you're eligible for.

One type of loan that is not normally talked about is an interest only loan. This type of loan allows you to make low monthly payments for a certain period, then the payment amount increases. These loans are generally used to help you get into a home at a low monthly payment.

You can request for the seller to pay for certain closing costs. For example, a seller can pay either a percentage of the closing cost or for certain services. Many times the seller is responsible for paying for a termite inspection along with a survey and appraisal of the property.

Try going with a short-term loan. Since interest rates have been around rock bottom lately, short-term loans tend to be more affordable for many borrowers. Anyone with a 30-year mortgage that has a 6% interest rate or higher could possibly refinance into a 15-year or 20-year loan while still keeping their the monthly payments near around what they're already paying. This is an option to consider even if you have slightly higher monthly payments. It can help you pay off the mortgage quicker.

Do not sign a home mortgage contract before you have determined that there is no doubt that you will be able to afford the payments. Just because the bank approves you for a loan does not mean that you could really endure it financially. First do the math so that you know that you will be able to keep the home that you buy.

Pay your credit cards on time if you are considering a home mortgage in the next few years. Your credit score and debt to income ratios will come into play when you go for a home mortgage. If you have multiple late payments or are carrying a lot of debt, you may find the mortgage offers you receive to be poor.

Be sure to compare the different term options that are available for home mortgages. You could choose between a number of options, including 10, 15 and 30 year options. The key is to determine what the final cost of your home will be after each term would be up, and from there whether or not you would be able to afford the mortgage each month for the most affordable option.

If you have filed for bankruptcy, you may have to wait two or three years before you qualify for a mortgage loan. However, you may end up paying higher interest rates. The best way to save money when buying a home after a bankruptcy is to have a large down payment.

Pay at least 20% as a down payment to your home. https://www.investorsobserver.com/news/stock-update/deutsche-bank-ag-db-stock-what-does-the-chart-say-friday will keep you from having to pay PMI (provate mortgage insurance) to your lender. If you pay less than 20%, you very well may be stuck with this additional payment along with your mortgage. It can add hundreds of dollars to your monthly bill.

There are times when the seller of a home will be able to give you a land contract so you can purchase the home. The seller needs to own the home outright, or owe very little on it for this to work. A land contract may need to be paid within a few years.

Never assume that a good faith estimate is fact or written in stone. It is in fact not just an estimate, but one written in good faith. Always be wary of extra costs and fees that can creep into the official and formal paperwork later that drive up your total expense.

Have a healthy and properly funded savings account prior to applying for a mortgage. You will need to have cash on hand for closing costs, a down payment and such miscellaneous expenses as inspections, application and credit report fees, title searches and appraisals. Of course, you'll get better mortgage terms if you have a larger down payment.

Look into foreclosed homes before you seek out properties that are brand new. Banks don't mind dealing with other banks, and they certainly prefer less expensive properties. If you can find a home that's offered for a great price, especially if the bank in question owns it, they will jump at the opportunity to have someone pick up the tab. It's a better option for them than auctions.

Be sure that you know exactly how long your home mortgage contract will require you to wait before it allows you to refinance. Some contracts will let you within on year, while others may not allow it before five years pass. What you can tolerate depends on many factors, so be sure to keep this tip in mind.

Now that you've read over this advice, you are ready to get out there and find the right mortgage for your home. You don't want to dive into this situation without the proper knowledge. Instead, you want to be able to make rational decisions along the way and get into the mortgage vehicle that works with you.